Open enrollment season is a crucial time for individuals to reassess their health insurance needs, especially for those with a history of hereditary conditions in their family. It presents an annual opportunity to switch plans, enhance coverage, or enroll in a new health insurance policy altogether. For those predisposed to genetic disorders, understanding how different plans cover these conditions is paramount. With the right approach, it's possible to secure coverage that adequately addresses the potential health risks associated with hereditary conditions.

During the open enrollment period, which typically runs from November 1 to December 15 in many countries, insurers cannot deny coverage based on pre-existing conditions, including hereditary ones. This is a critical time for evaluating your health insurance options, particularly if you have a family history of genetic disorders such as heart disease, diabetes, or cancer. According to the Centers for Disease Control and Prevention (CDC), about 10% of common diseases can be attributed to genetic factors, highlighting the importance of having a plan that covers genetic screenings and treatments.

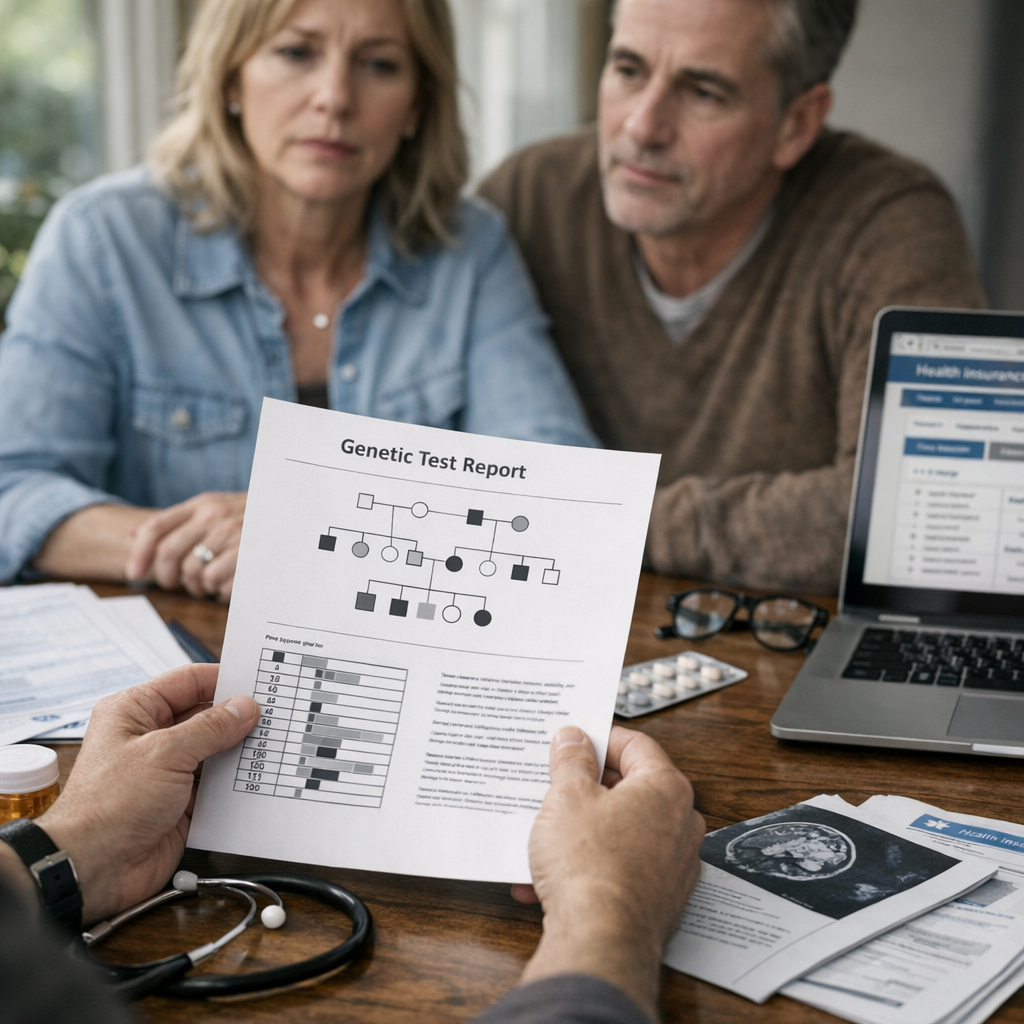

Key considerations should include checking if the health plan covers genetic testing, which can be a significant step in early detection and management of hereditary conditions. "As many as 1 in 4 individuals may carry genetic mutations that put them at increased risk for conditions like heart disease, cancer, and diabetes," notes a recent study published in the Journal of Genetic Medicine. When selecting a plan, look for terms like "genomic screening" and "family history" in the coverage details. Some plans may offer broader coverage for genetic counseling and testing, which can be crucial for preventive care strategies.

Moreover, reviewing out-of-pocket costs and coverage limits is essential, as treatments for hereditary conditions can be long-term and costly. The National Health Council reports that the average annual cost of treatment for chronic conditions can exceed $10,000, making comprehensive coverage a necessity for financial protection. Analyze deductibles, co-pays, and coinsurance to understand the full scope of what your financial responsibilities would be under each plan.

Finally, take advantage of resources available through your employer, health insurance marketplace, or independent advisors. They can provide personalized assistance and clarify complexities surrounding coverage options. Remember, the goal during open enrollment is not only to secure insurance that meets your health needs but also to ensure it is financially viable and comprehensive enough to cover potential treatments for hereditary conditions. With the right level of preparedness, you can navigate open enrollment effectively, ensuring peace of mind for the year ahead.