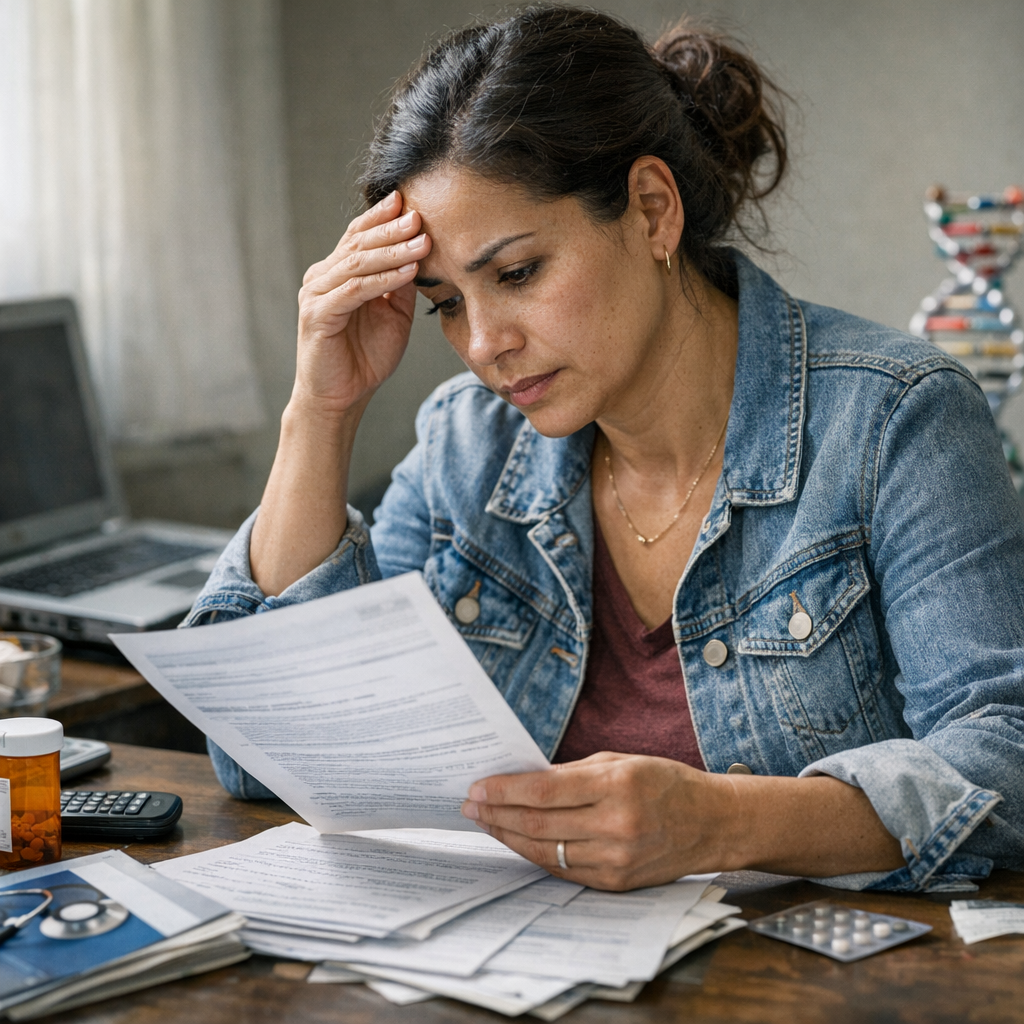

Understanding health insurance, especially for those with low income or genetic conditions that might affect coverage, is crucial in today's healthcare landscape. Individuals often face higher premiums or denial of coverage based on genetic predispositions to certain diseases. Recent legislative changes aim to protect such individuals, ensuring access to necessary and affordable healthcare. This guide will explore low-income health insurance options, the impact of genetics on insurance eligibility and costs, and how to navigate these challenges effectively.

For low-income individuals or families, the Affordable Care Act (ACA) provides subsidies to make health insurance more affordable. As of 2023, about 87% of ACA marketplace consumers received premium tax credits, reducing their monthly premiums substantially. Medicaid expansion under the ACA also increased accessibility; states that expanded Medicaid saw a significant decrease in uninsured rates among low-income adults, with rates dropping by over 13 percentage points since implementation. This expansion provides crucial coverage for many, including those with genetic conditions that might otherwise make health insurance unaffordable.

Genetic information can no longer be used to increase insurance premiums or deny coverage thanks to the Genetic Information Nondiscrimination Act (GINA) of 2008. GINA prohibits health insurers from using genetic information in underwriting decisions or considering it as a preexisting condition. This is particularly pertinent for low-income individuals who might not have been able to afford insurance due to potential genetic-related premium hikes. However, challenges remain as GINA does not apply to life insurance, long-term care, or disability insurance, showing the importance of comprehensive health coverage.

When considering health insurance options, low-income individuals should first determine their eligibility for Medicaid, which offers comprehensive coverage at little to no cost. For those slightly above the Medicaid income threshold, the ACA marketplace offers a sliding scale of subsidies based on income. It's essential to accurately report income and any known genetic conditions during the application process, as this can affect subsidy eligibility and the overall cost of insurance. Free or low-cost genetic counseling services may also be available through healthcare providers or advocacy groups, providing valuable information on managing health risks.

In conclusion, navigating the health insurance marketplace as a low-income individual with potential genetic health concerns can be daunting. Yet, understanding the protections and options available can significantly alleviate the burden. By leveraging Medicaid, ACA subsidies, and the protections afforded by laws like GINA, individuals can access the care they need. Staying informed, seeking assistance from healthcare navigators, and exploring all available options are key steps toward securing affordable and comprehensive health insurance coverage.