Understanding health insurance can be a daunting task, especially when factors like income and genetics play a significant role in the type of coverage you might need and qualify for. In the United States, low-income individuals and families may have access to subsidized plans through programs like Medicaid or the Affordable Care Act's (ACA) marketplace, which offer financial assistance based on income levels. Genetics, while not directly affecting eligibility for these programs, can influence the kind of health insurance coverage one might pursue, especially if there's a known risk of inherited conditions. This guide aims to unpack these complex interactions, providing clarity on how low-income individuals can secure health insurance that meets their unique genetic health needs.

For low-income families and individuals, navigating the maze of health insurance options begins with understanding the eligibility requirements for Medicaid and subsidized ACA plans. As of 2023, Medicaid eligibility in states that have expanded their program under the ACA includes adults with incomes up to 138% of the federal poverty level. Furthermore, the ACA marketplace offers sliding-scale subsidies for individuals and families with incomes between 100% and 400% of the federal poverty line. This financial assistance dramatically reduces premium costs, making health insurance more accessible for those with limited financial resources.

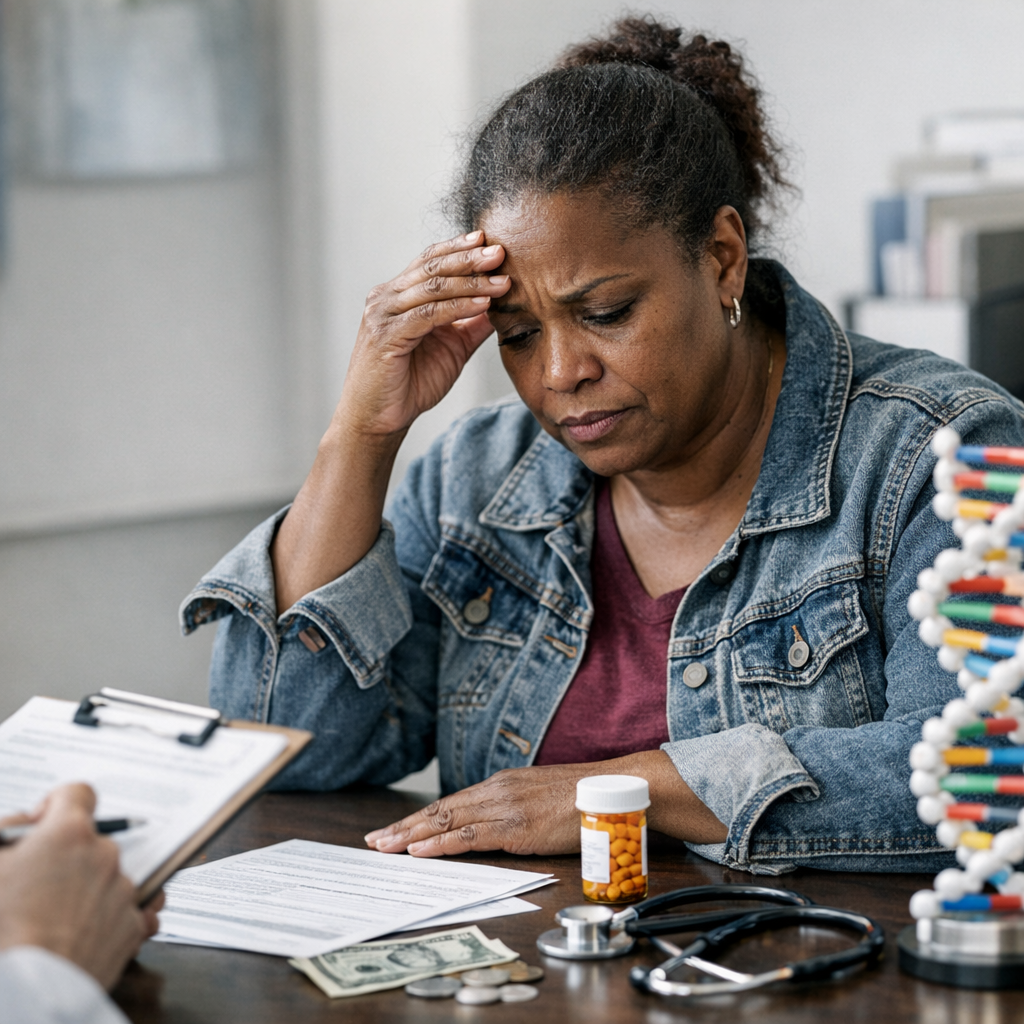

When it comes to genetics and health insurance, the Genetic Information Nondiscrimination Act (GINA) of 2008 plays a crucial role. GINA prohibits health insurers from discriminating against individuals based on their genetic information. This means that carriers cannot refuse to cover you or charge you more because you have a gene mutation that increases your risk for specific diseases. However, this protection does not extend to life insurance, long-term care insurance, or disability insurance. Individuals with a family history or predisposition to genetic conditions should consider this when exploring their health insurance options, ensuring they receive comprehensive coverage that accounts for potential needs.

Moreover, special considerations might be necessary for individuals with known genetic conditions. It's often recommended to look into health plans that offer broad specialist networks and cover genetic testing and counseling. According to the National Human Genome Research Institute, "Knowledge about the genetic predisposition to certain diseases can guide individuals in their health care decisions and risk management." In light of this, selecting a health insurance plan that covers preventive services and genetic counseling can be imperative for those at increased genetic risk. During the last open enrollment period, an estimated 8.3 million people selected plans through the ACA marketplace, highlighting the importance of these services for the broader population.

In conclusion, low-income individuals navigating the intricate landscape of health insurance should prioritize plans that cater not only to their financial situation but also to their unique health needs, including genetic predispositions. With the protections afforded by laws like GINA and the financial assistance available through Medicaid and the ACA marketplace, affordable and comprehensive health coverage is within reach. By focusing on plans that cover a wide range of services, including genetic counseling and testing, individuals can make informed decisions about their health care, ultimately leading to better health outcomes.