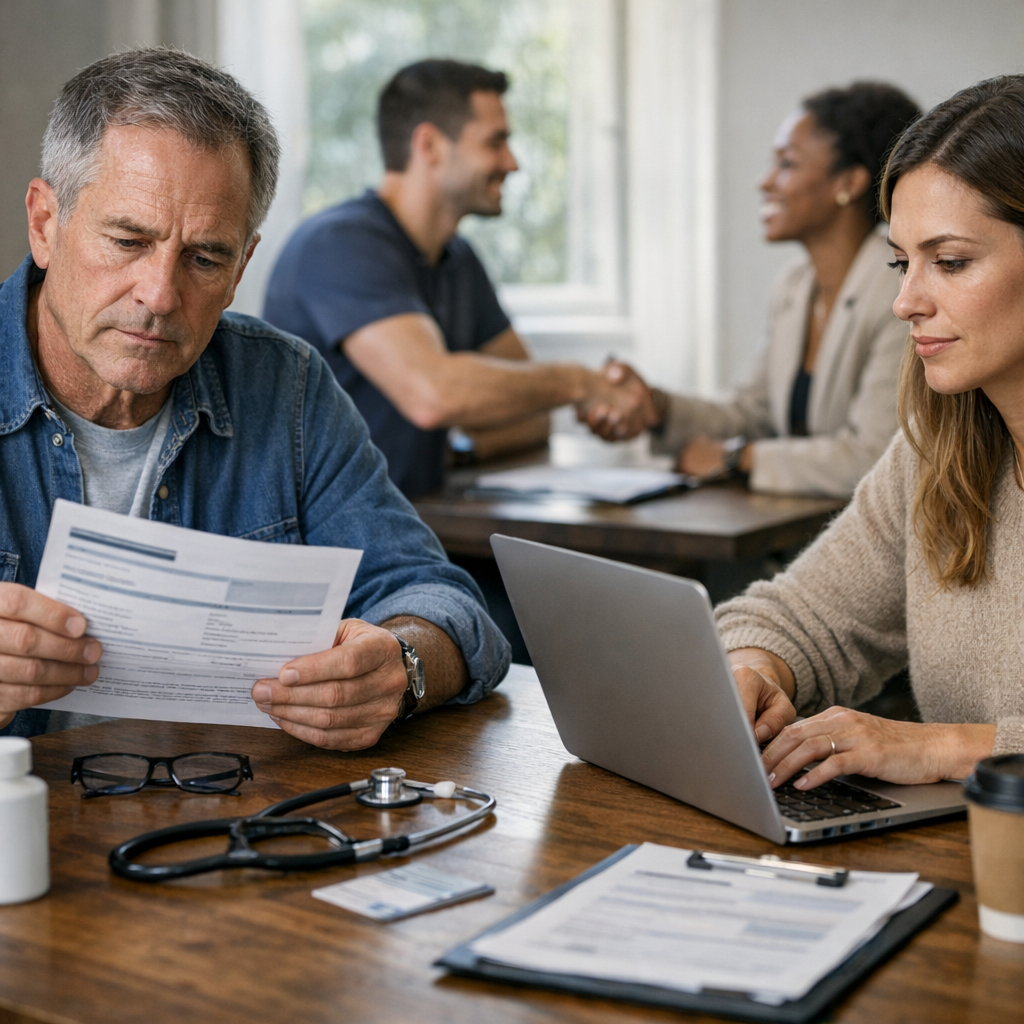

In the realm of health insurance, understanding the nuances of short-term health coverage and sponsorship can be key to effectively navigating your healthcare options. Short-term health insurance policies offer temporary coverage and can be an attractive option for individuals in transition—such as those between jobs, waiting for new job benefits to commence, or those who missed the enrollment period for traditional insurance. However, these policies are not without their caveats, often excluding pre-existing conditions and offering limited benefits compared to standard health insurance plans. Sponsorship, on the other hand, provides a pathway for individuals to receive health insurance through a sponsor, typically an employer or a family member, offering more comprehensive coverage but also requiring careful consideration of the terms and eligibility requirements.

Short-term health insurance, by design, is meant to be a stopgap solution, providing coverage for a period typically ranging from one to twelve months. According to the National Association of Insurance Commissioners, as of 2023, approximately 27% of those choosing short-term plans do so because they are waiting for other coverage to begin. The appeal of these plans lies in their lower premium costs; however, it's crucial to note that they often come with high deductibles and may not cover essential health benefits as defined by the Affordable Care Act (ACA).

Engaging in a health insurance sponsorship can significantly alleviate the financial burden of insurance costs, particularly for individuals and families eligible for employer-sponsored plans. A 2023 study by the Kaiser Family Foundation found that 49% of the U.S. population is covered by employer-sponsored health plans. These plans not only tend to offer more comprehensive coverage but also share the cost of premiums between the employer and the employee, making healthcare more accessible and affordable. Understanding the specifics of your sponsored plan, including coverage limits and network restrictions, is essential to maximizing its benefits.

When considering short-term health insurance or entering into a sponsorship agreement, it’s vital to assess your personal or family health care needs, understand the coverage details, and know the potential limitations and exclusions of the policy. For short-term insurance, always examine the fine print regarding pre-existing condition exclusions, coverage caps, and renewal policies. For those considering or being offered sponsorship, ensure that the plan aligns with your healthcare needs and that you understand your financial responsibilities under the plan. Consulting with a health insurance professional can provide personalized advice tailored to your situation, helping you make informed decisions about your health coverage.

In conclusion, both short-term health insurance and sponsorship offer valuable options for managing healthcare costs and ensuring coverage during times of transition or need. By carefully weighing the benefits, limitations, and terms of these options against your healthcare requirements and financial situation, you can make informed decisions that best suit your circumstances. Remember, the right choice will depend on your personal healthcare needs, the coverage options available to you, and the specifics of each plan.